Credit Card Basic Information (2025)

Know complete information about Credit Card Dates and Amount in India 2025

In today’s time, credit card has become a very important financial tool. Whether you need money for shopping, bill payments or emergency, credit card comes in handy everywhere. But if you do not know even the smallest thing and information about it, then its use can prove to be very dangerous and you can face a lot of problems.

In this article, we will tell you every little thing related to credit cards and explain some of its basic terms in simple words, such as billing cycle, bill date, due date, minimum amount due, total due and unbilled amount. Along with this, we will also give you complete information about the new changes that have come in 2025, which will help you in the coming time. There is a lot of information for you in this entire article, so you must read it completely.

1. What is Billing Cycle

Billing cycle is the time period in which you get the total of all the expenses you have made from your credit card in the form of a statement.

This cycle is usually of 30 days. As soon as the billing cycle is completed, the bank prepares your bill in which all your expenses and transactions, interest and charges are mentioned. Which makes it easy for you to understand the entire bill.

2025 update:

Now, some banks are offering such billing cycles that you can choose according to your convenience. This will make it easier for you to manage payments. And this will help you understand the bill easily by choosing according to your convenience.

2. What is Bill Date

Bill date is the day when your credit card statement is generated. All the money you have spent from the credit card till this date, all that appears in the statement. It has both total due and minimum due written on it. It is important to understand the bill date because according to that you have to think about paying the entire bill and plan when to pay the bill.

3. Meaning of Due Date

The due date is the last date till which you have to pay the credit card bill. If you do not pay the bill by this date then:

Late fees are levied

Extra interest charges are levied

Your credit score can be spoiled

Some new information has come in 2025:

RBI has told the banks that every user should be sent a reminder of the due date through SMS and email so that payment can be made on time. And no user forgets to make the payment and no user’s credit score or late charges are levied.

My opinion: I believe that RBI did a very good job by bringing this new rule because, due to this, when someone remembers his due date, he will remember and make the payment and due to this rule the credit score will also not be spoiled.

4. Meaning of Minimum Amount Due

Minimum amount due is the smallest amount which is deducted from your total credit card bill as a small part and if you are unable to pay the total due then you have to pay at least the minimum due. This keeps your account active and you do not go into default.

But if you pay only the minimum due then the remaining money will keep growing with interest. And this can trap you in a trap which you may face a lot of problems in getting out of.

So it is better that you pay as much amount as you can so that you can save interest.

My opinion : is that you should always try to clear the total outstanding due by any means because when we pay the total due, it has a very good impact on our credit score but if you repeatedly pay the minimum due, you may face a lot of problems and you may get caught in a trap which is very difficult to get out of and it also has a very bad impact on your credit score. In my opinion, you should always pay the total due.

2025 update:

Now banks will clearly show you in the bill how much interest you are getting and how much real money is outstanding.

5. What is the Total Amount Due

Total amount due is the full amount that you have used in the entire billing cycle – it includes purchases, interest, charges, and everything. The total amount due is made by combining all your expenses and charges and interest.

This is your actual outstanding which you should pay. Paying it timely increases your credit score and your credit limit as well, so you should pay it.

Improvement in 2025:

An option to view real-time total due is now being introduced in the mobile apps of banks. You can check at any time how much of your bill is pending. This helps you a lot.

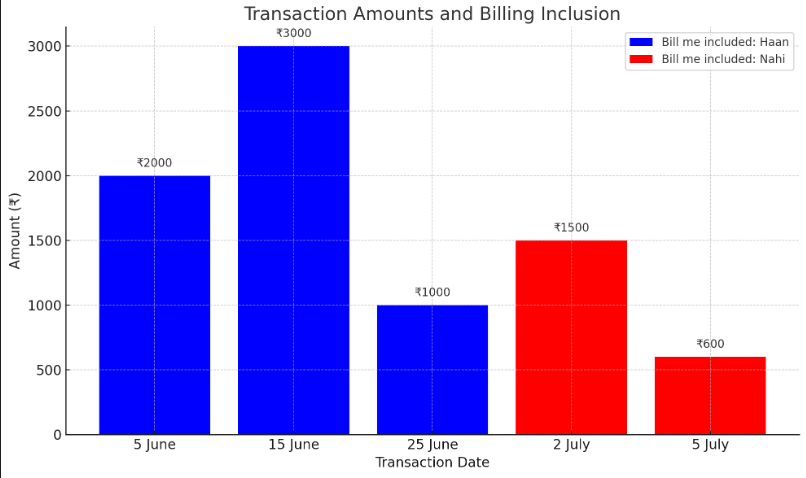

6. Meaning of Unbilled Amount

Unbilled amount is the money that you have spent after your billing cycle but is not yet showing in the current bill.

Example :

Suppose :

Your credit card billing cycle is from 1st June to 30th June.

Your bill date is 30th June.

And your due date is 20th July.

Now during this period, you made some transactions:

Transaction Summary Table

| Date | Transaction Details | Amount (₹) | Bill Me Included? |

|---|---|---|---|

| 5 June | Grocery shopping | ₹2,000 | Haan |

| 15 June | Online shopping (Amazon) | ₹3,000 | Haan |

| 25 June | Electricity bill | ₹1,000 | Haan |

| 2 July | Petrol | ₹1,500 | Nahi |

| 5 July | Movie tickets | ₹600 | Nahi |

So what do you understand?

All the transactions that happened between 1st June to 30th June (₹2,000 + ₹3,000 + ₹1,000 = ₹6,000), will all come in your bill on 30th June.

But whatever you spend after 30th June, like petrol on 2nd July or movie tickets on 5th July, will not be included in your current bill.

So what is the Unbilled Amount? Unbilled Amount are those transactions which are done after your billing cycle and are included in next month’s bill.

2025 Update About the Indian Banking and Credit Card Sector

The nature of banking and credit card scene in India starts taking impactful changes from now as we move forward to 2025. Some of the most important updates are as follows;

1. Increasing Billing Transparency

2025 will be a big year for pushing transparency in the credit card billing account. The Reserve Bank of India (RBI ) has made banks provide loud communication about the billing cycle and due date as well as charges configured. The objective is to give consumers a better sense of their financial commitment and prevent confusion over when a payment will be required.

2. Tracking Features in Real Time

Many banks are using real-time tracking features in their mobile banking applications to offer the necessary financial education and encourage responsible credit management efforts. These are the apps that provide users with checks on their spending, display unpaid balances, and notify the user of when their bills are coming. Built-in accessibility lets a consumer take control of their finances, and pay bills in a timely.

3. Better Customer Support

Given the value of customer service, banks are incorporating the best support processes for credit card users in a big way. Customers in 2025 will have faster response times, more available channels to ask questions, and will have support set up for dealing with billing disputes. The objective gets better since it would be an improvement to the credit card user experience.

4. Winner of the Financial Literacy Olympics

Now that digital banking is a thing, now more than ever financial literacy is integral. In 2025 consumer-facing banks promise to introduce new programs offering insights into credit card usage, the state of budgeting, and understanding what debt management entails These will likely feature online webinars, educating webinars, and user-friendly tools to aid the consumer in managing their finances wisely.

5. New and Better Rewards Programs

IN 2025, credit card issuers will have to get more creative when designing rewards programs to tap and keep customers These could come in the form of individualized rewards, percentage cashback on certain baskets, and pro-arrangement rotations with many popular brands. Through specific rewards to consumer needs, banks will strive to generate a better experience and persuade high satisfaction (and loyalty of sorts).

6. Stronger Security Processes

Banks are focusing on defense as cyber threats keep growing, this will be seen in what credit card solutions provide in the future. Consumers can look forward to a more robust 2025 with new features like biometric authentication, virtual card numbers for online transactions, and real-time transaction notifications. These measures are there to protect the consumers and ensure a secure transaction.

7. Regulatory Changes

Credit Card regulations in India are also going through big changes due to the new regime. They will soon introduce stricter rules that are going to shield consumers from money-lending practices and firm treatment. Among the elements set by regulation are interest rates and fees, and clarity of terms and conditions. Those changes impinge on consumers: keep abreast of them, and keep an eye on their rights and responsibilities as credit card users.

8. Ease of access

Banks will be encouraged by the government, to extend credit card privileges to a larger section of the population in India in the next six years as part of its financial inclusion program. This will be given with the subtext of extending credit or allowing the unbanked and scoreless access to a consumer credit card. Access expansion is designed to enable more consumers to become incorporated into the formal financial system, and equip them with a credit profile.

9. Digital-first Method

Digital banking has come a long way making the credit card ecosystem relationship shift significantly with consumers. In 2025, you will get full-on topline digital-first services like the ability to apply for a credit card online, bank accounts that are user-friendly, and contactless payments. It is not only to make things convenient but also this is because India is a country full of tech-savvy population.

Use Credit Cards in the Right Way

Now that we have covered the subtle modifications, it becomes vital to frequent responsible credit card habits for better financial health. Here are a few simple ways to manage your credit card in the right way:

1. Learn Your Billing Cycle: You should know when you are receiving a bill from your credit card and its due date so you can watch your bill date and pay date. Do this to avoid paying late and late fees.

2. Pay on Time: Aim to pay your total due no later than the due date. At the least pay the minimum, to avoid extra charges. You will always be on the safe side of no late payments with automatic payments.

3. Keep an Eye on Your Spending: You do this in real-time via your banking app. This will help you stick to your budget and keep from overflowing on anything.

4. Educate yourself: Take advantage of online resources that the banking and financials provide for improving finance literacy. You can be an empowered decision-maker if you know how credit works, and interest rates + fees;

5. Reward-conscious: If your credit card provides rewards or cashback, do use them sensibly; Select a card that matches your spending to take full advantage of the benefits.

6. Credit Limit Management: Never use more than 30% of available credit, this is your sweet creditworthiness goal. Heavy utilization can be bad for your creditworthiness.

7. Handle/New credit Carefully: It would be easy to have lots of applications open for credit card rewards, but.. too many triggers are a danger right now.

8.Multiple Time Apply: Applications and tracking of multiple accounts may set a trap for you as each application will affect your credit score.

9. Informative: You will want to stay on top of the credit card industry as it changes with new features, regulations, and best practices. The best defense against the potential perils of consumer credit is knowledge.

My opinion

You can check this amount by going to your bank app and seeing it in real-time, so that you have an idea of how much your next bill would be.

All these transactions will appear in the next month’s statement. But you can see them in advance in the bank app.

If you track the unbilled amount, you will have an idea of what the approximate bill for the next month could be. This makes budgeting easy, which helps you a lot.

Conclusion

Based on the projection for 2025, the credit card industry in India is going to have a complete transformation. With the scope of increased transparency, support for customers and enhanced financial education consumers are more able to deal with credit. By understanding the basics of credit cards and staying informed about the latest updates, you can make responsible financial decisions that contribute to your overall well-being.

Whether you’re using credit cards for everyday purchases, building your credit history, or enjoying rewards, remember that responsible usage is key. With the right knowledge and habits, you can leverage credit cards as a valuable financial tool while avoiding common pitfalls. Embrace the changes in the banking sector and take charge of your financial future in 2025 and beyond.

Most Important Topic Post in India 2025

{kind=link}

{kind=link}

{kind=link}